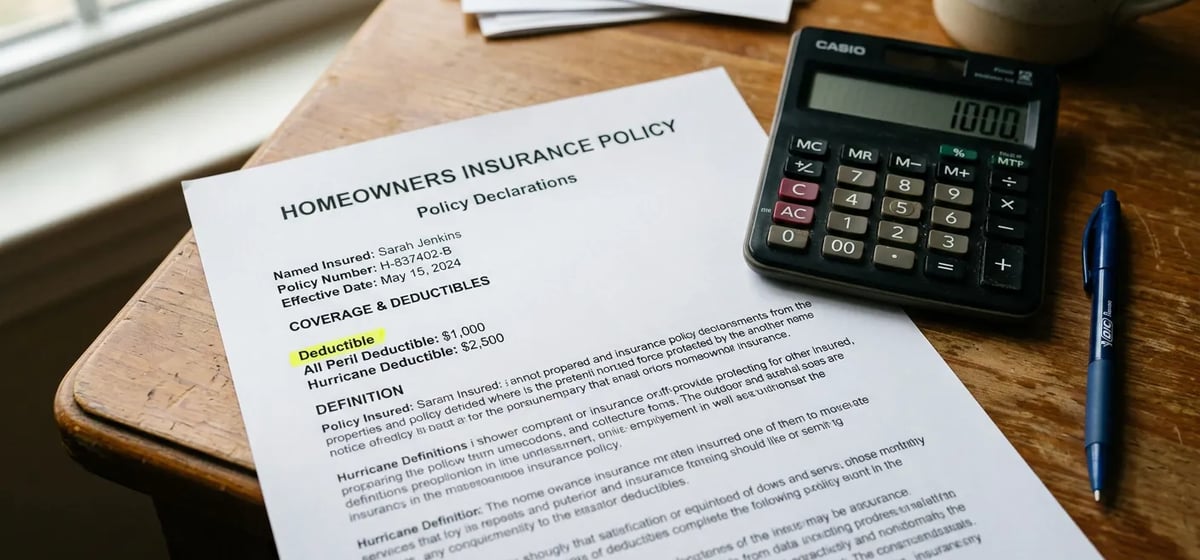

What Is a Deductible?

A deductible is the exact amount of money you must pay out of pocket before your home insurance steps in to cover a claim. Think of it as your shared portion of the risk. If a bad storm damages your house, the insurance company doesn't pay for the whole repair right away. You pay your set amount first. Then, the insurance company pays the rest up to your policy limit. You'll find this amount clearly listed on the front page of your Home Insurance paperwork. This front page is called the declarations page. You choose this amount when you buy your policy. It's one of the most important financial choices you make for your home.

Flat Rates and Percentages

Insurance companies usually offer two main types of deductibles. The first type is a flat rate. This is a specific dollar amount that stays the same no matter what happens. Common flat rate deductibles run from 500 to 2,500 dollars. If a heavy tree branch falls on your garage and causes 10,000 dollars in damage, and you have a 1,000 dollar flat deductible, you pay 1,000 dollars. The insurance company pays the remaining 9,000 dollars.

The second type is a percentage deductible. This is based on the total insured value of your home, not the cost of the damage. You see this most often with wind, hail, or hurricane damage in coastal states. If your home is insured for 300,000 dollars and you have a 2 percent wind deductible, you must pay 6,000 dollars before the insurance kicks in. This can be a massive financial surprise if you need major Roofing repairs after a summer storm. Always check your paperwork to see if you have special percentage rules for named storms or earthquakes.

Why Your Deductible Matters

Your deductible directly affects your monthly insurance bill. This monthly or yearly bill is called your premium. If you choose a low deductible like 500 dollars, your monthly bill will be higher. The insurance company takes on more risk because they have to pay out sooner, so they charge you more upfront. If you choose a high deductible like 2,500 dollars, your monthly bill goes down. You take on more risk, so the insurance company gives you a break on the price. Over time, choosing a higher amount can save you hundreds of dollars a year.

When to File a Claim

You shouldn't file an insurance claim for every little thing that breaks around the house. You only want to use your insurance for large disasters. If a repair costs less than your deductible, the insurance company won't pay anything at all. However, the claim will still go on your official record. Having claims on your record can make your future insurance rates go up or even get your policy canceled.

For example, say a local plumber charges 800 dollars to fix a leaky pipe and patch the wall. If your deductible is 1,000 dollars, you pay the whole 800 dollars yourself. The insurance pays nothing. You should just pay the plumber directly and leave the insurance company out of it. You want to save your insurance for major Home Emergencies. These massive repairs can easily cost 15,000 to 50,000 dollars or more, though ranges vary by area. Good times to file a claim include:

- A massive tree crushing your roof and breaking your trusses.

- A grease fire destroying your kitchen cabinets and appliances.

- A burst main water line flooding your entire finished basement.

In those cases, paying your 1,000 dollar share makes perfect sense.