What is a contingency?

The word traces back to the Latin word contingere. That means to happen or befall. Lawyers began using the term in contracts to cover unexpected events that might happen before a deal is finished. In real estate, a contingency is a safety clause written into your purchase contract. It acts as a shield when you are Buying a Home.

When you make an offer on a house, you usually hand over an earnest money deposit. This deposit proves you are a serious buyer. Earnest money typically runs 1 to 3 percent of the home price. On a $400,000 house, that means you put down $4,000 to $12,000. A contingency says that certain conditions must be met for the sale to go through. If those conditions are not met, you can walk away from the deal. Best of all, you get to keep your earnest money deposit.

Why contingencies matter to you

Contingencies protect your wallet and your peace of mind. Without them, you are legally locked into buying the house no matter what goes wrong. If you sign a contract without any safety clauses, you take on all the risk.

Imagine you discover the house has severe termite damage right before closing. Without a contingency, you cannot back out without losing your entire deposit. The seller could even sue you for breaking the contract. Contingencies give you a legal way to cancel the purchase without a penalty.

They also give you power to negotiate. If a problem pops up, you do not always have to walk away. You can use the contingency to ask the seller to fix the issue. You can also ask them to lower the price or give you a credit at closing.

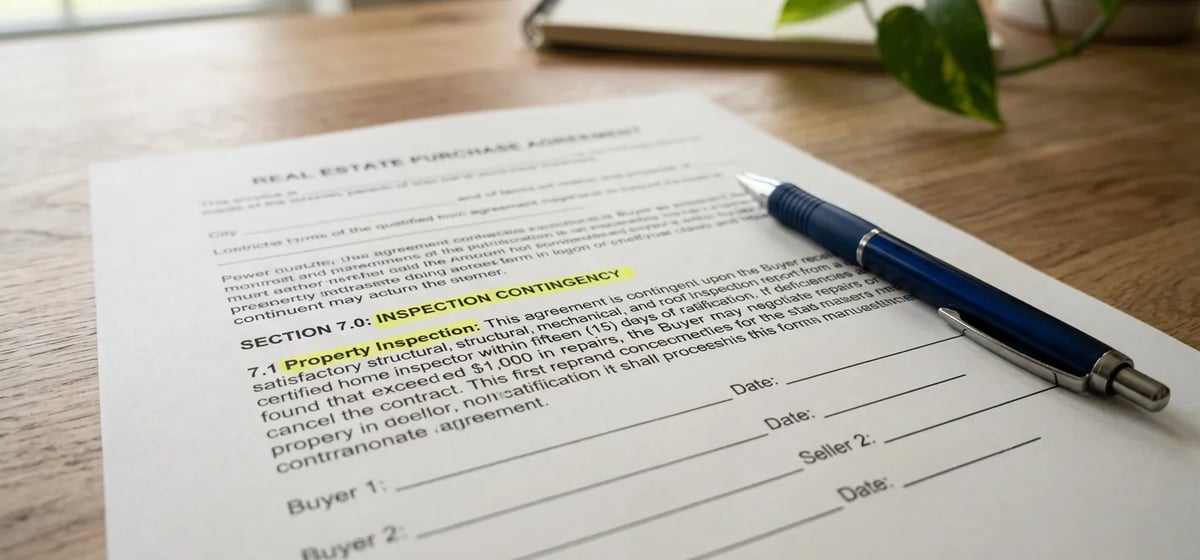

Common types of contingencies

Most standard real estate contracts include a few basic safety clauses. Here are the ones you will see most often.

- Inspection contingency: This gives you a set number of days to hire a professional home inspector. A standard home inspection costs $300 to $500, though prices vary by region. If the inspector finds major problems with the Foundation & Structure, you can cancel the deal or demand repairs.

- Appraisal contingency: Your bank wants to ensure the house is actually worth the money you agreed to pay. They will hire an appraiser to check the value. If the appraisal comes in lower than your offer price, you can back out or ask the seller to drop the price.

- Financing contingency: This clause says your purchase depends on your bank officially approving your loan. Even if you already have pre-approval for Mortgages, final approval can take weeks. If the bank denies your loan at the last minute, this clause lets you walk away safely.

- Home sale contingency: If you already own a house, you might need to sell it before you can afford a new one. This clause says you will only buy the new house if your current house sells first.

What to watch for

Contingencies only protect you if you follow the rules of the contract. Every safety clause comes with a strict deadline. You might have 10 days to finish your inspection and 21 days to secure your loan. If you miss a deadline by even one day, you lose your protection. You must keep close track of these dates.

Warning: In a very competitive housing market, a seller might ask you to waive your contingencies to make your offer look better. This is incredibly risky. If you waive your inspection contingency and later find out the house needs a $15,000 roof replacement, you have to pay for it yourself.

Always talk to your real estate agent or lawyer before you agree to remove a contingency. They will help you weigh the risks. A strong offer is great, but protecting your life savings is much more important.