What Is a Mortgage?

A mortgage is a massive loan you use to buy a house. The bank pays the seller. You pay the bank back over a set number of years. The house acts as collateral. If you stop paying, the bank can take the house back. When you are buying a home, you sign a stack of papers that legally binds you to this deal. During your first month as a homeowner, setting up autopay for this loan is the smartest move you can make.

The Anatomy of Your Monthly Payment

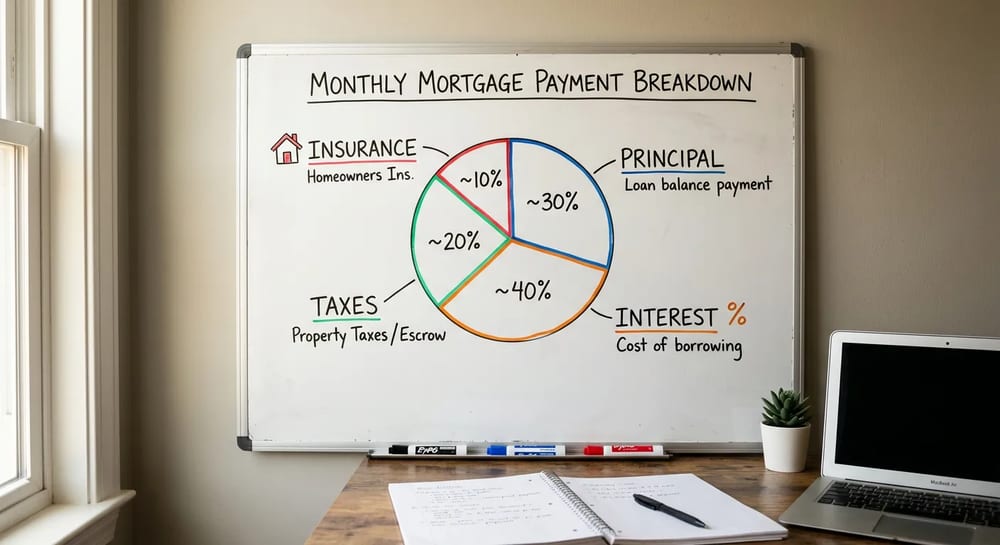

Your monthly payment isn't just paying back the money you borrowed. It covers four main buckets. Lenders call this PITI. It stands for Principal, Interest, Taxes, and Insurance.

- Principal: The actual money you borrowed to buy the house.

- Interest: The fee the bank charges you to borrow that money.

- Taxes: Your local property taxes.

- Insurance: Your home insurance policy. It might also include private mortgage insurance if you put down less than 20 percent.

How Amortization Works

This is the hardest part for new homeowners to swallow. Your monthly payment stays the exact same for 30 years. But the way that money gets split up changes every single month. This process is called amortization.

In the early years, almost all your money goes to interest. The bank takes their profit first. Only a tiny slice pays down your actual loan balance. By year 15 or 20, the math flips. You finally start making huge dents in the principal.

Note: These dollar amounts are rough examples based on a 2,000 dollar payment. Actual costs vary widely by region, scope, and home age.

The Mystery of the Escrow Account

An escrow account is basically a forced savings account managed by your lender. You pay a little bit toward your taxes and insurance every month. The bank holds that cash in escrow. When your tax bill or insurance premium is due, the bank pays it for you.

This protects the bank. They know the house won't burn down uninsured or get seized for unpaid taxes. Your escrow payment changes every year because property taxes and insurance rates change. This is why your total monthly payment goes up even if you have a fixed interest rate. Read more about managing this in our guide to property taxes and home finances. If you live in the home as your primary residence, a homestead exemption can lower the property tax portion of that escrow payment.

How Much House Can You Afford?

Before you fall in love with a listing, you need a real number. Lenders decide how much they will lend using two simple rules of thumb. They are often called the 28/36 rule. Your total housing payment should stay under 28 percent of your gross monthly income. All your debt payments combined, including the mortgage, car loans, and credit cards, should stay under 36 percent.

That 36 percent figure is your debt-to-income ratio, or DTI. It is the single most important number a lender looks at. A mortgage calculator or affordability estimator is really just doing this math for you. It takes your income, your debts, the interest rate, and the loan length, then spits out a monthly payment and a maximum home price. Our dedicated mortgage calculator page walks through a full payment breakdown and a refinance estimator.

Estimating Your Own Payment

You do not need a fancy tool to ballpark a payment. Here is the manual version most loan officers use to sanity-check a budget.

- Write down your gross monthly income, before taxes are taken out.

- Multiply that number by 0.28. This is the most a comfortable total housing payment should be.

- Add up your existing monthly debt payments (car, student loans, credit cards).

- Multiply your income by 0.36, then subtract your debts from step three. The result is another safe ceiling for the mortgage.

- Use the lower of the two numbers as your target monthly payment, then work backward to a home price.

Remember that the payment includes more than principal and interest. Property taxes, home insurance, and possibly private mortgage insurance all live inside that monthly number. A house that looks affordable on the sticker price can blow past your budget once a high local tax bill is added in.

| Gross Monthly Income | 28% Housing Ceiling | Rough Max Payment (with debts) |

|---|---|---|

| $4,000 | $1,120 | $1,000 to $1,120 |

| $6,000 | $1,680 | $1,500 to $1,680 |

| $8,000 | $2,240 | $2,000 to $2,240 |

| $10,000 | $2,800 | $2,500 to $2,800 |

One last warning about the numbers a calculator gives you. The bank will often approve you for far more than the 28 percent rule suggests is comfortable. Just because you qualify for a payment does not mean you should take it. Leaving room in your budget for repairs, savings, and life is what keeps a home from becoming a burden.

Fixed vs Adjustable Rates

Most people get a 30 year fixed mortgage. The interest rate never changes. Your principal and interest payment is locked in forever. A 15 year fixed mortgage works the same way, but you pay it off twice as fast. Your monthly payment is higher, but you save tens of thousands of dollars in interest.

An adjustable rate mortgage has a low rate for the first few years. Then the rate changes based on the economy. If rates go up, your monthly payment goes up.

| Loan Type | Rate Stability | Monthly Payment | Best For |

|---|---|---|---|

| 30 Year Fixed | Never changes | Lowest | Long term stability |

| 15 Year Fixed | Never changes | Highest | Paying off debt fast |

| 5/1 ARM | Changes after 5 years | Starts low, then varies | Selling before year 5 |

Types of Mortgage Loans

The fixed-versus-adjustable choice is about the interest rate. But mortgages also fall into different categories, or loan programs, based on who backs the loan. These categories decide your down payment, your credit requirements, and the fees you pay. Picking the right one can save you thousands or open the door to a house you thought was out of reach.

There are two big buckets. Conventional loans are not backed by the government; they follow rules set by Fannie Mae and Freddie Mac. Government-backed loans (FHA, VA, and USDA) carry a federal guarantee that lets lenders accept lower credit scores and smaller down payments.

| Loan Type | Typical Down Payment | Credit Friendliness | Best For |

|---|---|---|---|

| Conventional | 3% to 20% | Needs solid credit | Buyers with good credit and savings |

| FHA | As low as 3.5% | Accepts lower scores | First-time buyers, thinner credit |

| VA | Often 0% | Flexible | Eligible veterans and service members |

| USDA | Often 0% | Moderate | Buyers in qualifying rural areas |

| Jumbo | 10% to 20%+ | Needs strong credit | High-priced homes above local limits |

A few notes that trip people up. FHA loans require mortgage insurance for most of the life of the loan, which a conventional loan lets you drop once you reach 20 percent equity. VA and USDA loans can require zero money down, but VA charges a one-time funding fee and USDA only works inside designated areas. A jumbo loan is simply any loan too large to qualify as conventional under the local lending limit; it is not a separate government program.

Choosing the Right Program

- Check your credit score first. It steers which programs you even qualify for and the rate you will be offered.

- Add up your cash for a down payment and closing costs. Low cash points you toward FHA, VA, or USDA.

- Confirm eligibility for the special programs. VA needs military service; USDA needs an eligible address.

- Compare the all-in cost, not just the rate. A low rate with heavy mortgage insurance can cost more than a slightly higher rate without it.

- Ask two or three lenders for a written Loan Estimate so you compare the same numbers side by side.

Country matters here too. The FHA, VA, and USDA programs are United States loan types. Canadian buyers work within a different system that includes mortgage default insurance through providers like CMHC when the down payment is under 20 percent. The core idea is the same, but the program names and rules differ by country. When you are buying a home, ask a local lender which programs apply where you live.

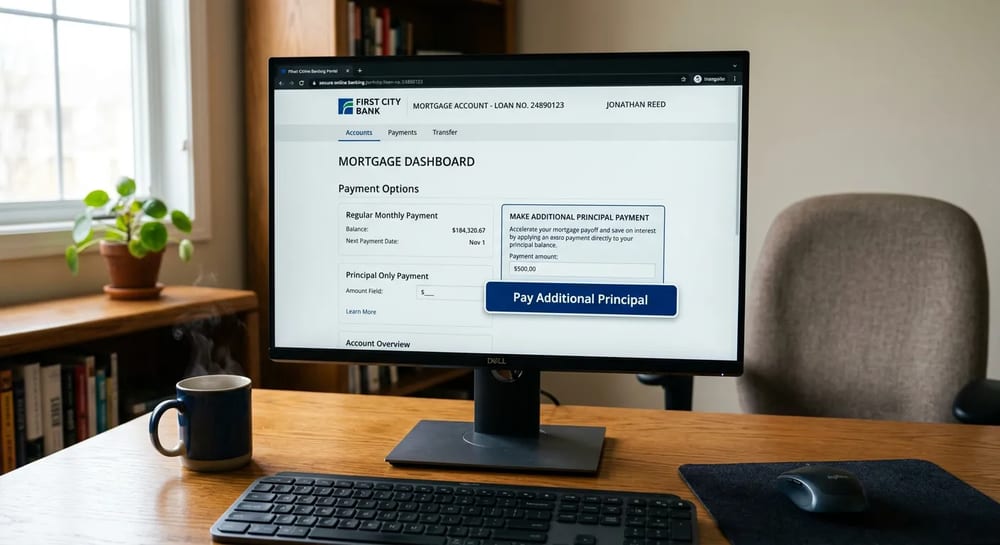

Extra Payments and Paying It Off Early

You can pay your loan off faster by adding extra money to your monthly payment. Even an extra 50 to 100 dollars a month shaves years off your loan. Because of the way amortization works, extra payments hit your principal directly. You skip the interest charge on that money entirely.

Refinancing Your Mortgage

Refinancing means replacing your current home loan with a brand new one. The new loan pays off the old one, and you start fresh with new terms. Homeowners refinance for two main reasons: to lower their interest rate and monthly payment, or to pull cash out of the equity they have built up. Whether it actually pays off comes down to the break-even math, so before you refinance, read our full mortgage refinance guide, which walks through the types, the costs, and when to skip it.

A rate-and-term refinance swaps your loan for one with a better rate or a different length, like moving from a 30 year loan to a 15 year loan. A cash-out refinance gives you a bigger loan than you owe and hands you the difference in cash, which homeowners often use for a major repair or to pay off high-interest debt.

When Refinancing Makes Sense

Refinancing is not free. You pay closing costs all over again, usually 2 to 5 percent of the loan amount. To know if it is worth it, you find your break-even point: divide the total closing costs by your monthly savings. If the costs are 4,000 dollars and you save 200 dollars a month, you break even in 20 months. If you plan to stay in the home past that point, refinancing pays off.

- Check current rates against your existing rate. A drop of around three quarters of a percent or more often makes a refinance worthwhile.

- Estimate your closing costs by asking a lender for a Loan Estimate.

- Calculate your break-even point in months.

- Compare that to how long you actually plan to keep the house.

- Decide whether lower payments, a shorter term, or cash in hand is your real goal.

| Refinance Type | What It Does | Best For |

|---|---|---|

| Rate-and-term | Lowers rate or changes loan length | Cutting your monthly payment |

| Cash-out | Borrows against your equity for cash | Funding a big repair or consolidating debt |

| Shorter-term | Moves you to a 15 year loan | Paying off the home faster |

Refinancing also resets your amortization clock. If you are ten years into a 30 year loan and refinance into a new 30 year loan, you stretch your payoff back out to 40 years total. You may lower the payment, but you could pay more interest over time. Compare the lifetime cost, not just the monthly number. Closing costs and rules vary by region, lender, and home value, so get quotes from more than one lender before signing.

What Happens If You Miss a Payment?

Life happens. If you can't make your payment, don't ignore it. Call your lender immediately. Most banks give you a 15 day grace period. After that, they charge a late fee. The fee is usually 3 to 6 percent of your monthly payment.