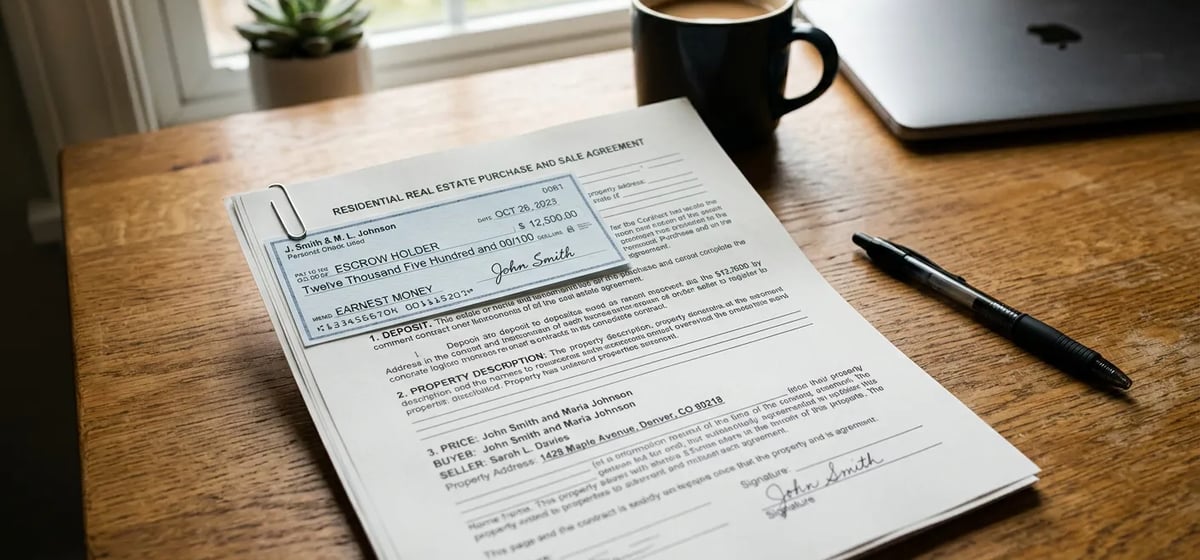

What is Earnest Money?

When you make an offer on a house, the seller wants to know you're serious. This is where earnest money comes in. The word earnest comes from the Old English word eornost. It means seriousness or genuine intent. Real estate professionals often call this a good faith deposit. It's a cash payment you make right after the seller accepts your offer. This money proves you plan to follow through with the purchase.

How Much Do You Pay?

The amount you pay depends on your local real estate market. In a normal market, you can expect to put down 1 percent to 3 percent of the purchase price. For a $400,000 home, that equals $4,000 to $12,000. In a very competitive market where many buyers want the same house, sellers might expect 5 percent to 10 percent. Exact ranges vary based on where you live and how fast homes are selling. You'll usually write a personal check, get a certified bank check, or send a wire transfer within a few days of signing the contract.

Where Does the Money Go?

You don't hand this money directly to the seller. That would be risky. Instead, the money goes to a neutral third party. This is usually an escrow company, a title company, or a real estate broker. They hold your deposit in a safe trust account while you work on buying a home.

The money sits there while you handle your inspections, get your appraisal, and finalize your loan. Once closing day arrives, the money doesn't just disappear. It belongs to you. The escrow company applies your earnest money toward your total down payment or your closing costs. If your total cash needed at closing is $50,000 and you already paid $5,000 in earnest money, you only need to bring $45,000 to the closing table.

How to Protect Your Deposit

You might wonder if you can lose this money. The short answer is yes, but only if you break the rules of your contract. You protect your deposit by using contract contingencies. These are special clauses that let you walk away from the deal and get your money back if something goes wrong.

Most standard real estate contracts include three main contingencies:

- Inspection contingency: You get your money back if a home inspector finds major problems like a bad roof or cracked foundation and the seller refuses to fix them.

- Appraisal contingency: You get your money back if the home appraises for less than your offer price and you can't reach a new agreement with the seller.

- Financing contingency: You get your deposit back if you can't get final approval for mortgages or other loans.

What Happens If the Deal Cancels?

Sometimes a home purchase doesn't work out. If you cancel the contract for a valid reason covered by your contingencies, the escrow company will refund your money. Both you and the seller must sign a cancellation document. Once everyone signs, the title company cuts you a check or wires the funds back to your bank account. This process usually takes a few days to a week.

If the seller decides they no longer want to sell the house, they can't just keep your money. They must return your deposit. In some cases, if the seller breaks the contract, they might even owe you additional damages. However, if you simply wake up one morning and decide you don't like the house anymore, you're out of luck. Breaking the contract without a valid contingency means you forfeit the cash. The seller keeps your deposit as compensation for the time their house was off the market.