What is a peril?

In the insurance world, a peril is a specific event that causes damage to your home or belongings. The word comes from the Latin word periculum, which means danger or risk. Insurance companies use this word to define exactly what hazards they will pay to fix. When a tree falls on your house or a burglar steals your TV, the event that caused the loss is the peril. Understanding this term helps you know exactly how your home insurance protects you.

Named vs. open perils

Home insurance policies usually handle these risks in one of two ways. You'll either have a named peril policy or an open peril policy.

A named peril policy only covers the exact events listed in your contract. If a risk is not on that list, your insurance won't pay for the damage. An open peril policy works the opposite way. It covers every possible risk except for the ones specifically listed as exclusions. Open peril policies offer broader protection, but they usually cost more money.

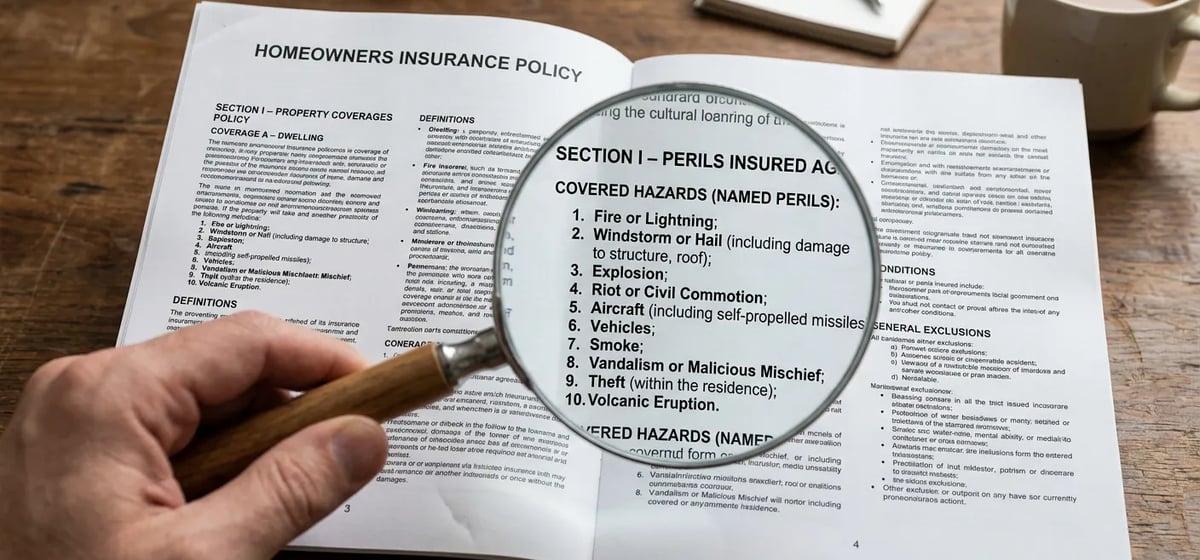

Covered and excluded events

Most standard home insurance policies cover a very similar list of common risks. Here are the events you'll usually see covered:

- Fire and smoke damage

- Windstorms and hail

- Theft and vandalism

- Lightning strikes

- Sudden plumbing bursts

These events can cause incredibly expensive damage. A minor kitchen fire might cost 3,000 to 5,000 dollars to fix, while a major house fire can cost 50,000 to 150,000 dollars. Replacing a roof after a bad hail storm typically costs 10,000 to 20,000 dollars. Keep in mind that these ranges vary widely based on your home size and location. Having coverage for these home emergencies keeps you from paying those huge bills out of pocket.

It's just as important to know which risks your policy leaves out. Almost all standard policies exclude certain major disasters.

Other common exclusions include general wear and tear, mold, pest damage, and sewer backups. If termites destroy your wall studs, your insurance company considers that a maintenance issue rather than a sudden covered event. You are expected to keep up with routine maintenance to prevent these slow problems.

Perils and deductibles

Sometimes your insurance company will charge a different deductible depending on the specific event that caused the damage. A deductible is the amount of money you have to pay out of your own pocket before your insurance starts paying.

For most common risks like fire or theft, you'll pay your standard flat deductible. This is usually a set amount like 1,000 to 2,500 dollars. But for severe weather events, your policy might use a percentage deductible instead.

If you live near the coast, you might have a separate deductible for hurricane or windstorm damage. This is often 1 to 5 percent of your total home coverage limit. If your house is insured for 400,000 dollars and you have a 2 percent windstorm deductible, you'll have to pay 8,000 dollars out of pocket before the insurance kicks in to fix your roofing or siding. Always check your policy to see if certain risks trigger these higher deductibles.

How to check your policy

You should know exactly what risks your policy covers before disaster strikes. Pull out your insurance declarations page. This document summarizes your coverage. Look for sections labeled Coverage A for your main house structure and Coverage C for your personal property.

Read through the fine print to see if you have named or open coverage. Many policies use open coverage for the physical house structure but use named coverage for the belongings inside. If you live in an area prone to hurricanes or wildfires, double check that your policy doesn't exclude those specific events. If you find gaps, call your agent to ask about adding extra coverage.