The True Cost of Owning

When you are buying a home, the monthly mortgage payment is only part of the math. You also have to pay property taxes, insurance, and maintenance costs. Together, these extra expenses can add hundreds or even thousands of dollars to your monthly budget.

Understanding these costs keeps you out of financial trouble. It stops surprise bills from ruining your month. You need to know how your taxes are calculated and where your escrow money goes.

How Property Taxes Work

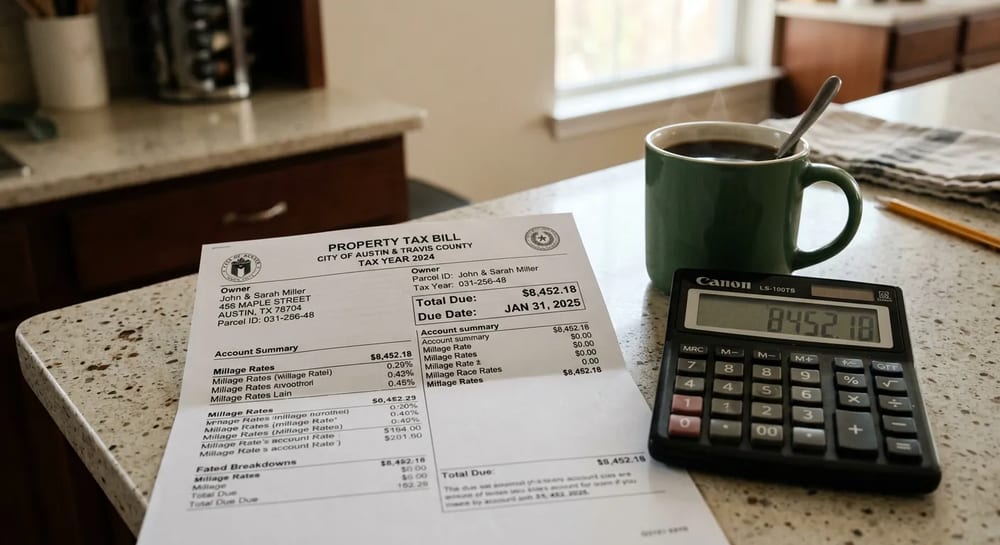

Local governments use property taxes to pay for schools, roads, and emergency services. The amount you pay depends on two things. First is the assessed value of your home. Second is the local tax rate, which is often called a millage rate.

The assessed value is not the same as the market value. Market value is what a buyer would pay for your house today. Assessed value is a number the local tax office assigns to your property. In many places, the assessed value is lower than the market value.

Your local tax office updates this value on a set schedule. Some towns do it every year. Others wait three to five years. When your assessed value goes up, your tax bill usually goes up too.

Appealing Your Tax Assessment

Tax assessors make mistakes. They might think your home has three bathrooms when it really only has two. They might value your home much higher than identical houses on your street. If you think your assessed value is too high, you can appeal it.

Winning an appeal lowers your tax bill. The process usually works like this.

- Read your assessment notice carefully. It will list a strict deadline for filing an appeal.

- Look for factual errors on your property card. Check the square footage, bedroom count, and lot size.

- Find three to five similar homes in your neighborhood that sold recently for less than your assessed value.

- Fill out the appeal form and submit your evidence before the deadline.

Understanding Your Escrow Account

Most lenders require you to have an escrow account. This is a special holding tank for your money. Each month, you pay a portion of your annual property taxes and home insurance along with your mortgage. The lender puts that extra money into the escrow account.

When your tax bill or insurance premium is due, the lender pays it for you using the money in the escrow account. This protects the lender. It ensures the house does not get seized for unpaid taxes or destroyed in a fire without insurance coverage.

Escrow accounts are not perfect. Your tax and insurance costs change over time. This leads to two common situations.

Escrow Shortages

If your taxes or insurance rates go up, your escrow account will not have enough money to pay the bills. This is a shortage. Your lender will pay the difference, but they want that money back. They will raise your monthly mortgage payment for the next year to make up the difference.

Escrow Overages

Sometimes your taxes go down, or you switch to a cheaper insurance policy. In this case, your escrow account collects too much money. By law, the lender must send you a refund check for the extra amount once a year.

Budgeting for Routine Maintenance

Houses constantly break. You need a dedicated cash fund for repairs. Financial experts often suggest the one percent rule. This means you should save one percent of your home value every year for maintenance.

If your home is older or in harsh weather, you might need two percent to four percent. For a home worth $300,000, saving one percent means setting aside $3,000 a year, or $250 a month.

Here is how annual maintenance costs scale based on a conservative 1.5 percent estimate.

Planning for Big Ticket Items

Routine maintenance covers small things like clogged drains and peeling paint. Capital expenditures are the massive replacements. Every major system in your house has a lifespan. When they die, you have to replace them.

You need to know the age of your roof, your heater, and your appliances. Start saving for replacements years before they break. Hiring contractors for these big jobs requires serious cash.

Below is a rough guide to the lifespan and replacement costs of common major systems. Keep in mind that these price ranges vary widely by region, the scope of work, and the age of your home.

| System | Average Lifespan | Estimated Replacement Cost |

|---|---|---|

| Asphalt Shingle Roofing | 15 to 25 years | $6,000 to $12,000 |

| HVAC (Furnace and AC) | 12 to 20 years | $5,000 to $10,000 |

| Water Heater | 8 to 12 years | $1,000 to $2,500 |

| Exterior Paint | 7 to 10 years | $2,500 to $5,000 |

| Kitchen Appliances | 10 to 15 years | $2,000 to $5,000 |

The Property Tax Appeal Process Step by Step

An appeal almost always starts informal and only goes formal if that fails. Knowing the order saves you time. Most homeowners win at the first step and never reach a hearing.

- Read your assessment notice the day it arrives. It states your new assessed value and the exact deadline to challenge it. Miss that date and you wait a full year.

- Pull your property card from the county portal. Confirm the square footage, bedroom and bathroom counts, lot size, and any listed features. A single wrong number can inflate your value.

- Gather three to five comparable sales. Look for homes near you with similar size, age, and condition that sold for less than your assessed value.

- Request an informal review with the assessor. Many offices fix clear errors at this stage with a phone call or a short meeting.

- File a formal appeal if the informal review fails. You present your evidence to a review board or tribunal. Bring your comparable sales and any photos of needed repairs.

The Homestead Exemption and Other Tax Breaks

A homestead exemption lowers the taxable value of your primary residence. It removes a set dollar amount or a percentage from your assessed value before the tax rate is applied. The result is a smaller bill on the home you actually live in. You can read more in the homestead exemption guide.

This break usually applies only to your main home, not a rental or a vacation property. Many places require you to file a one time application to claim it. Once approved, it often renews automatically.

Homestead is not the only relief available. Local governments offer several other programs.

- Senior exemptions: Extra reductions or value freezes for owners above a certain age.

- Veteran exemptions: Reduced taxable value for current and former service members, sometimes larger for service related disabilities.

- Disability exemptions: Relief for owners with a qualifying disability.

The rules, dollar amounts, and deadlines vary widely by state and province. Check your local assessor or revenue office for the programs you qualify for.

How Home Improvements Affect Your Taxes

Big improvements can raise your assessed value. A finished basement, an added bathroom, or a new deck gives the assessor a reason to value your home higher. A higher value usually means a higher tax bill. Routine repairs, like fixing a leak or repainting, rarely move the number.

Improvements also matter when you sell. The money you spend on permanent upgrades adds to your cost basis, which is roughly what the home is worth for tax purposes. A higher cost basis can reduce the capital gain, the profit, that you might owe tax on at sale.

The line between a repair and an improvement, and the way gains are taxed, depends on your local rules and your situation. Treat this as general background and confirm the details with a tax professional before you sell.

Building Home Equity

Equity is the part of your home you truly own. It equals the current value of the property minus the balance you still owe on the mortgage. If your home is worth $400,000 and you owe $250,000, you have $150,000 in equity.

Equity grows in two main ways. Each monthly payment retires a slice of the loan principal, so the amount you owe shrinks over time. The home itself can also rise in value, called appreciation, which lifts the value side of the equation. Extra payments toward principal speed the process up.

Once you have built equity, you can borrow against it. Two common tools do this.

- HELOC: A home equity line of credit works like a credit card tied to your house. You draw cash as needed up to a limit and pay interest only on what you use.

- Cash out refinance: You replace your existing mortgage with a larger one and take the difference in cash. This resets your loan terms and rate.

Both options use your home as collateral, so falling behind on payments puts the property at risk. Build equity steadily and borrow against it with care.