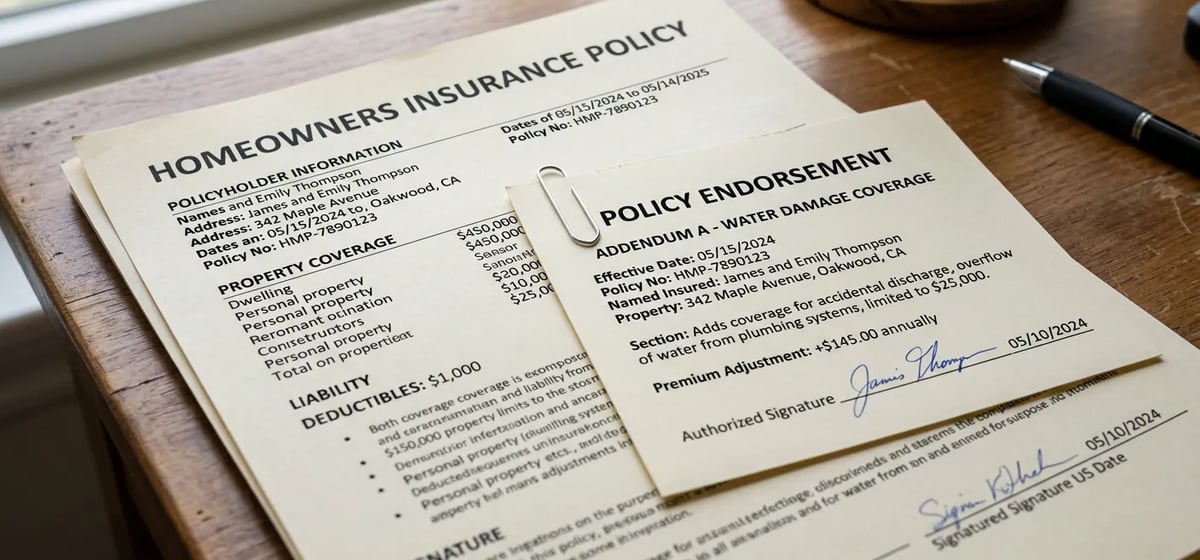

What is an endorsement?

When you buy a standard Home Insurance policy, you get a basic package of protection. But basic coverage doesn't fit every house. An endorsement is a legal document that changes your main policy. It adds, removes, or alters your coverage. Insurance companies also call these riders or floaters. You pay a little extra on your premium to get this specific protection. The word comes from a Latin phrase meaning to put on the back. It originally referred to writing a signature or a new rule on the back of a paper contract.

Why you might need one

Standard insurance caps how much it'll pay out for certain items. For example, a basic policy might only pay out 1500 dollars for stolen jewelry. If you have an engagement ring worth 5000 dollars, you need an endorsement to cover the full value.

Endorsements also cover events that standard policies ignore. A normal policy covers water damage from a burst pipe inside your walls. But it won't pay a dime if a city sewer line backs up into your basement. You need a specific endorsement for water and sewer backups. If your home has aging Plumbing, this extra coverage is a lifesaver.

Common endorsements and ballpark costs

Adding an endorsement is usually much cheaper than buying a whole separate policy. Costs depend heavily on where you live and the value of your items. Keep in mind that price ranges vary widely by state.

Here are a few common endorsements you might see:

- Scheduled personal property: This covers expensive items like wedding rings, art, or musical instruments. It usually costs 1 to 2 dollars for every 100 dollars of value. Insuring a 5000 dollar ring might cost you 50 to 100 dollars a year.

- Water backup coverage: This pays for damage if a sump pump fails or a drain backs up. It is incredibly common and usually costs 50 to 250 dollars a year.

- Building code upgrades: If your house is older, repairing it after a fire means you have to bring it up to modern building codes. Standard insurance only pays to replace what was there before. This endorsement covers the extra cost of the new codes. It usually adds about 10 percent to your base premium.

- Equipment breakdown: This covers major home systems if they fail from electrical or mechanical issues. It acts like a home warranty and usually costs 25 to 50 dollars a year.

How to add an endorsement to your policy

You don't have to wait until your policy renews to add an endorsement. You can call your insurance agent any time to adjust your coverage. If you buy a new piece of expensive jewelry or upgrade your home, call your agent that same week.

For high value items, your insurance company will ask for an appraisal or a detailed receipt. They need proof of what the item is worth before they agree to cover it. Make it a habit to review your policy during Your First Year as a Homeowner and every year after that. This ensures your endorsements still match what you own.

What to watch for

Endorsements are helpful, but they have strict rules. You must read the fine print. An endorsement for a home business might cover your computer equipment, but it might not cover liability if a client trips on your front steps.

Also, be careful not to double up on coverage. Sometimes a home warranty covers the exact same things as an equipment breakdown endorsement. You don't want to pay twice for the same protection. Finally, remember that endorsements have deductibles. If you have a water backup endorsement, you might still have to pay the first 500 dollars out of pocket before the insurance kicks in. Always ask your agent exactly how the deductible works for each new piece of coverage you buy.