What is a policy exclusion?

A policy exclusion is a specific rule written into your home insurance contract. It points out exactly what the insurance company will not cover. The word comes from the Latin word excludere, which means to shut out. Insurance companies use these rules to clearly define the boundaries of the financial risk they are willing to take. When you buy a policy, you might think it covers everything that could go wrong. It does not. Every policy has a list of events or types of damage that are completely shut out from coverage.

You will usually find these rules listed in a specific section of your Home Insurance paperwork. Reading this section helps you understand exactly what you are paying for. If an excluded event damages your house, the insurance company will not write you a check. You will have to pay for the repairs yourself.

Why it matters to you

Knowing your exclusions matters because it protects your wallet. If a pipe bursts and floods your kitchen, standard insurance usually pays. But if heavy rain floods your neighborhood and water enters your home, standard insurance will not pay. That is a standard exclusion. Repairing a flooded first floor can easily cost 20,000 to 50,000 dollars out of pocket. Prices always vary by location and damage, but the financial hit is huge.

If you do not know your exclusions, you might face a massive bill during an emergency. Another common exclusion involves your home structure. Most policies exclude damage caused by earth movement. If the ground shifts and cracks your concrete slab, you will pay for the repairs. You can read more about how to spot these issues in our guide to Foundation & Structure.

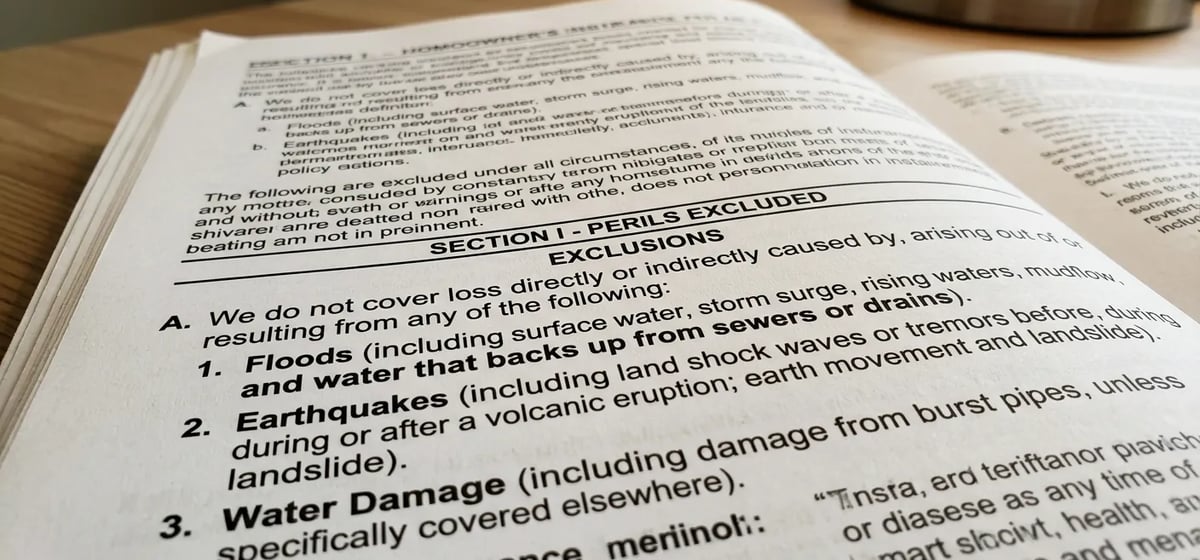

Common exclusions to watch for

Insurance companies across the US share a very similar list of exclusions. They refuse to cover slow damage that you could have prevented. They also refuse to cover massive natural disasters that affect entire cities at once.

- Flooding: Water that comes from the ground up, like heavy rain or overflowing rivers, is never covered by a standard policy.

- Earthquakes and landslides: Any damage from the earth moving is excluded.

- Pest infestations: Damage from termites, mice, or carpenter ants is your responsibility. You can learn how to handle these bugs in our Pest Control guide.

- Wear and tear: If your roof simply gets old and leaks, the insurance company will not buy you a new one. They expect you to maintain your home.

- Mold: Unless a covered accident caused the mold, companies usually exclude mold removal.

How to fill the gaps

You do not have to live with these gaps in your protection. You can buy extra coverage to override many exclusions. This extra coverage is called an endorsement or a rider. You can also buy completely separate policies for major disasters.

For example, you can buy a separate flood insurance policy through the National Flood Insurance Program. A typical flood policy costs 500 to 1,500 dollars a year. Costs range widely depending on your local flood zone. If you live in California, you can buy a separate earthquake policy. If you have expensive jewelry, you can add a rider to cover it, since standard policies exclude high value items. Talk to your insurance agent about the specific risks in your zip code. They can help you buy the right add-ons to keep your home fully protected.